Why Buy and Hold Real Estate Is Your Path to Long-Term Wealth

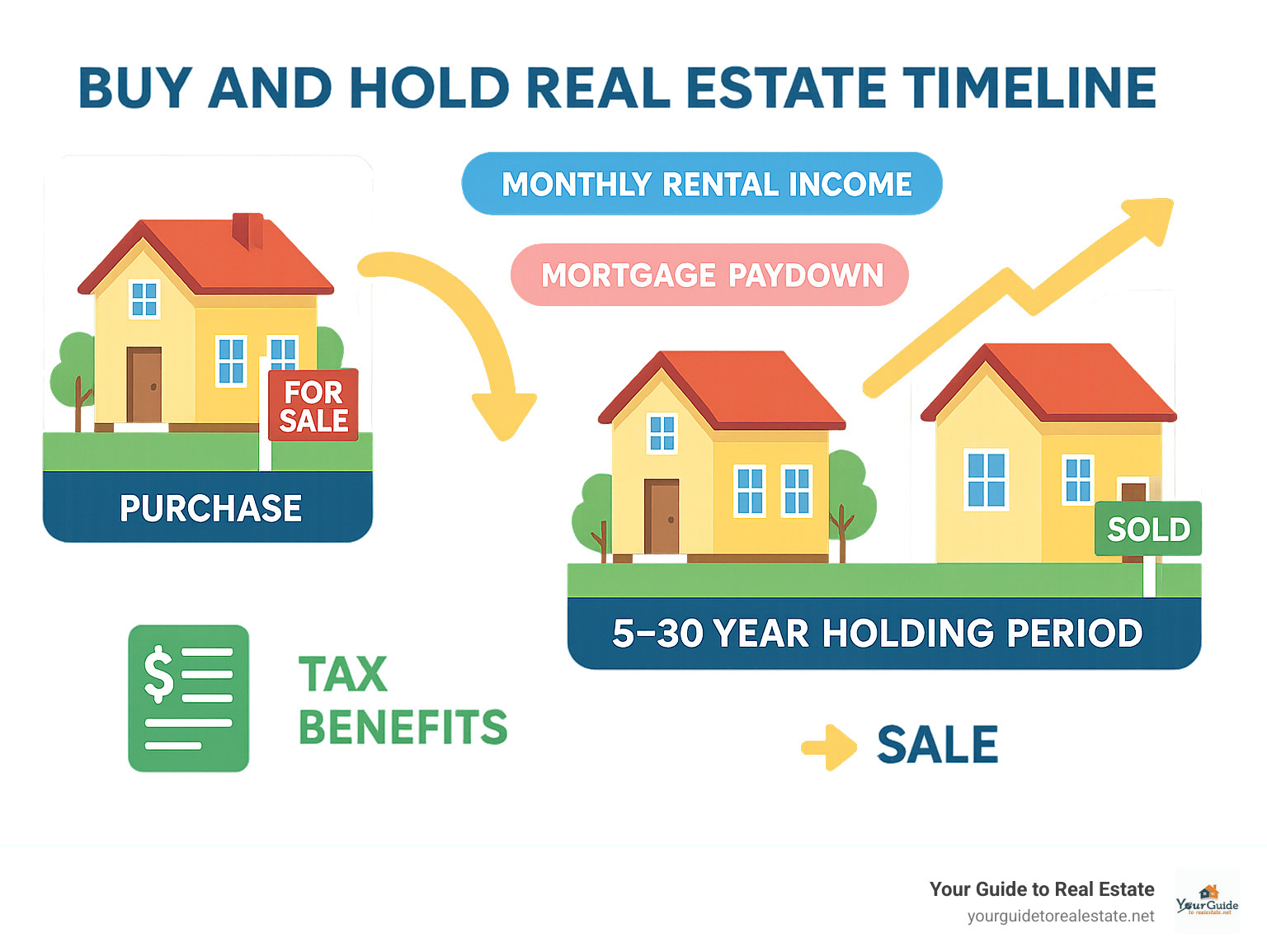

Buy and hold real estate is a simple investment strategy where you purchase rental properties and keep them for years (typically 5-30 years) to earn monthly rental income while the property appreciates in value over time.

Quick Answer for Buy and Hold Real Estate:

- What it is: Purchase property → Rent it out → Hold long-term → Sell when ready

- Timeline: 5-30 years (minimum 1 year for tax benefits)

- Income sources: Monthly rent + property appreciation

- Best for: Patient investors wanting passive income and wealth building

- Returns: 4-10% from rental income alone, plus appreciation

Warren Buffett once said, “Our favorite holding period is forever.” This mindset captures the essence of buy and hold investing perfectly.

The median U.S. home price increased by 238% over the past 20 years, while many buy and hold properties generate 4-10% returns from rental income alone. When you combine monthly cash flow with long-term appreciation, you get a powerful wealth-building machine.

Unlike flipping houses or wholesaling deals, buy and hold investing rewards patience over expertise. Your tenants help pay down your mortgage while inflation pushes both property values and rents higher over time.

Easy buy and hold real estate word list:

– how to invest in property strategy

– how to invest in real estate

– invest in real estate online

What Is Buy and Hold Real Estate Investing?

Buy and hold real estate investing is beautifully simple: you purchase a property, rent it out to tenants, and keep it for years while building wealth two ways at once. Your tenants pay monthly rent that covers your expenses plus gives you cash flow, while your property appreciates in value over time.

The typical holding period ranges from 5 to 30 years, though some investors never sell their best properties. The longer you hold, the more powerful this strategy becomes thanks to compound growth and inflation working in your favor.

You have two main paths when starting out:

Turnkey properties are rental-ready homes needing minimal work. You’ll pay a premium for convenience, but it’s perfect if you want to start collecting rent immediately.

Value-add properties require some work upfront – fresh paint, new flooring, or updated fixtures. You’ll pay less initially but invest time and money getting them rent-ready.

Buy and Hold Real Estate Basics

The magic happens through three wealth-building forces working simultaneously. Tenant rent covers your property expenses and provides positive cash flow each month.

Leverage amplifies your returns dramatically. When you put 20% down and finance the rest, a 5% increase in property value gives you a 25% return on your actual cash invested.

Equity pay-down happens automatically. Every month, part of your tenant’s rent payment goes toward your mortgage principal. After 15-30 years, you could own the property free and clear.

How the Strategy Works Day-to-Day

Rent collection happens mostly on autopilot with online platforms automatically transferring money from your tenant’s account to yours.

Maintenance requests pop up occasionally. You can handle simple fixes yourself or build relationships with reliable contractors.

Smart investors keep cash reserves equal to 1-3 months of property expenses for unexpected repairs or vacancy periods.

Many successful investors eventually hire a property manager to handle tenant communications and maintenance coordination, changing their investment into truly passive income.

Key Benefits of a Buy and Hold Strategy

When you choose buy and hold real estate, you’re creating multiple income streams from a single investment. It’s like planting a tree that gives you fruit every month while growing bigger each year.

Monthly cash flow is money that lands in your bank account after paying your mortgage, taxes, insurance, and maintenance costs. Even $200-300 per property adds up to real money when you own multiple properties.

Property appreciation is where real wealth building happens. Between 2001 and 2020, while inflation crept up by 41.26%, median home prices shot up by 238%. Your property didn’t just keep pace with rising costs – it crushed them.

The tax benefits are incredible. The IRS lets you deduct mortgage interest, property taxes, maintenance costs, and even depreciation. For detailed information about capital gains, check out Tax Topic No. 409 (capital gains).

Principal pay-down means your tenants are paying down your mortgage for you. Over 30 years, this adds up to hundreds of thousands of dollars in equity.

Buy and hold real estate acts as a powerful inflation hedge. When everything else gets more expensive, your fixed-rate mortgage payment stays the same while rents and property values climb.

Snowball Effect on Net Worth

As your properties appreciate and you pay down mortgages, you’re building equity that becomes the key to expanding your portfolio. You could potentially pull out equity through refinancing to use as down payments on additional properties.

This snowball effect is how ordinary people build extraordinary wealth. Each property helps you buy the next one.

Inflation-Proofing Your Portfolio

Inflation is actually your friend when you own rental properties. When inflation heats up, rent escalations follow while your mortgage payment stays frozen in time. Meanwhile, property values climb right along with the Consumer Price Index.

The Federal Reserve’s housing data consistently shows that real estate outpaces inflation over the long term.

Risks, Drawbacks & Proven Mitigations

Buy and hold real estate comes with real risks that can impact your returns. Illiquidity means you can’t quickly sell like stocks – real estate typically takes 2-6 months to sell with 6-10% transaction costs.

Vacancy periods are inevitable. Every time a tenant moves out, you’ll face weeks without rental income while still paying expenses. Budget for 1-3 months of vacancy per year.

Tenant issues can be stressful. Even with thorough screening, you might get tenants who pay late, damage property, or require expensive evictions.

Capital expenditures surprise you at the worst times. HVAC systems, roofs, and water heaters all have expiration dates that can cost $5,000-$15,000 to replace.

Market downturns remind us that real estate doesn’t always go up. The 2008 financial crisis showed how quickly property values can plummet.

Stress-Testing Your Numbers

Before buying any property, ask tough questions: What if rents drop 10%? What if vacancy jumps to 20%? What if you face $10,000 in unexpected repairs?

Your cash-on-cash return should still make sense in these scenarios. For detailed guidance on running these numbers, our guide on Valuation and Market Analysis in Real Estate walks you through the process.

Compliance & Landlord Laws

Becoming a landlord means real legal responsibilities. Fair housing laws are federal requirements with serious penalties if violated. Security deposit regulations and eviction procedures vary by location.

In places like Ontario, the Residential Tenancy Act governs every aspect of landlord-tenant relationships. Ignorance of local laws can be financially devastating.

Treat these challenges as business expenses rather than deal-breakers. Build risks into your calculations and develop systems to minimize their impact.

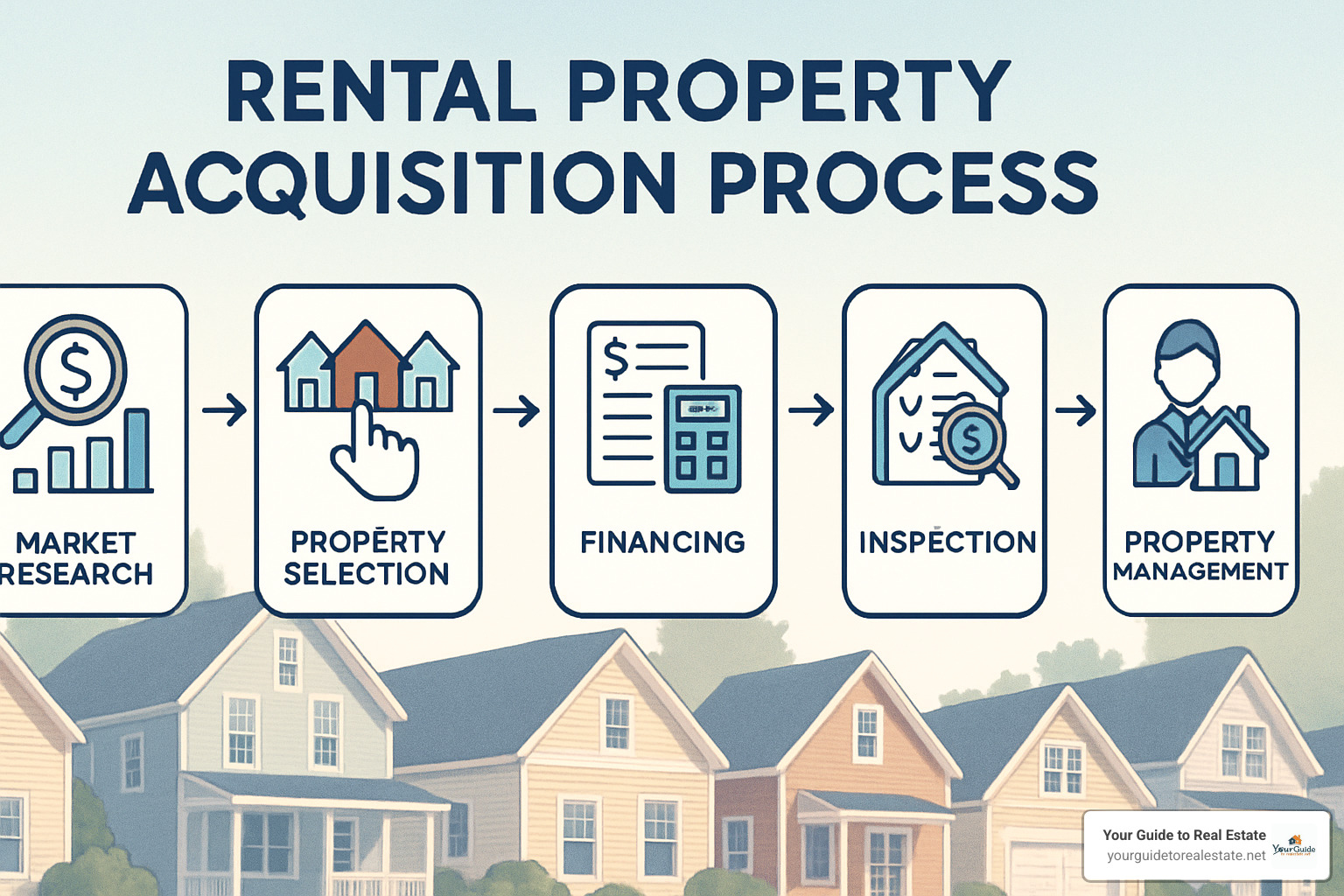

Step-by-Step Guide to Acquiring & Holding a Property

The buy and hold real estate process starts with deal sourcing – finding properties that make financial sense through real estate websites, driving neighborhoods, and building agent relationships.

Underwriting means analyzing every number: purchase price, repair costs, monthly rent potential, taxes, insurance, and ongoing expenses. You’re creating a business plan for this property.

Financing typically involves conventional loans with 20-25% down payments. Getting pre-approved helps you move quickly on good deals.

Many properties need rehab work before they’re rent-ready. Budget carefully – repair costs can quickly eat into projected returns.

Management begins once your property is ready for tenants. You’ll need systems for tenant screening, rent collection, maintenance requests, and accounting.

Exit planning might seem premature, but smart investors always have an exit strategy. Understanding your long-term goals guides decisions throughout the holding period.

1. Property Selection & Market Research

Choosing the right property and market is your foundation. Start by looking at job growth in your target area. Cities adding jobs consistently attract new residents who need housing.

Population growth goes hand-in-hand with job growth. When more people move to an area, housing demand increases, pushing both property values and rents higher.

Use the rent-to-price ratio test: divide monthly rent by purchase price. Generally, you want 1% or higher, though this can be challenging in expensive markets.

Look for neighborhoods with good schools, reasonable commute times, and amenities like parks and shopping. Areas with higher percentages of renters often indicate strong rental markets.

For a deeper dive into analyzing markets, our guide on Competitive Market Analysis Real Estate walks you through the process.

You’re not just buying a property – you’re buying into a community and local economy. Take time to understand both.

2. Financing Options Explained

Conventional mortgages are where most investors start. Investment properties require 20-25% down and credit scores of at least 620-680. Interest rates are usually slightly higher than primary residence loans.

Portfolio lenders keep loans in-house instead of selling to Fannie Mae or Freddie Mac. They often offer more flexible terms and may accept lower credit scores.

DSCR loans (Debt Service Coverage Ratio loans) qualify you based on whether the property itself generates enough income to cover mortgage payments, not your W-2 income.

Private money comes from individuals or companies lending their own money, often at 8-12% interest but with much more flexibility and faster closing times.

Partnerships can help if you have good credit but limited cash, or vice versa.

Buy and Hold Real Estate vs. Flipping

Flipping houses requires hands-on management, construction knowledge, and good market timing. Profits get taxed as ordinary income.

Buy and hold real estate is more passive, building sustainable wealth through monthly cash flow and long-term appreciation. Profits qualify for lower capital gains tax rates.

Buy and Hold Real Estate vs. BRRRR

BRRRR (Buy, Rehab, Rent, Refinance, Repeat) emphasizes rapid portfolio growth by refinancing within 6-12 months to pull out invested capital.

Traditional buy and hold is more patient, focusing on steady cash flow and letting natural market appreciation build wealth over time.

3. Landlord Operations & Tenant Care

Good tenants are like gold – they pay on time, take care of your property, and stay for years.

Tenant screening is your first defense. Verify that potential tenants earn at least three times the monthly rent in income. Check credit scores (aim for 600+), call their employer, and contact their previous landlord.

Your lease agreement is your legal protection. Make sure it clearly spells out rent due dates, late fees, repair responsibilities, and property rules. Have a local attorney review your lease template.

Maintenance systems can make or break your experience. Build relationships with reliable contractors before you need them. Respond to maintenance requests within 24 hours.

Technology tools like Buildium, Rent Manager, or Cozy can handle rent collection, maintenance requests, and expense tracking automatically.

Decide whether to self-manage or hire a property management company (typically 8-12% of monthly rent). Self-managing saves money but requires your time. Professional management makes your investment truly passive.

4. Knowing When & How to Sell

Deciding when to sell your buy and hold real estate can be tricky since the strategy is built around holding for years.

Sell when a property stops making financial sense – maybe the neighborhood has declined or you’re facing major capital expenditures that don’t justify the returns.

Market conditions matter too. If property values have far outpaced rents, you might be sitting on a goldmine worth harvesting.

Tax Considerations are crucial. Properties held for more than one year qualify for long-term capital gains tax rates (0%, 15%, or 20%) instead of ordinary income tax rates (22%, 32%, or higher).

1031 Exchanges let you defer capital gains taxes entirely by reinvesting sale proceeds into another investment property. You must identify replacement properties within 45 days and complete the exchange within 180 days, but it’s an incredibly powerful wealth-building tool.

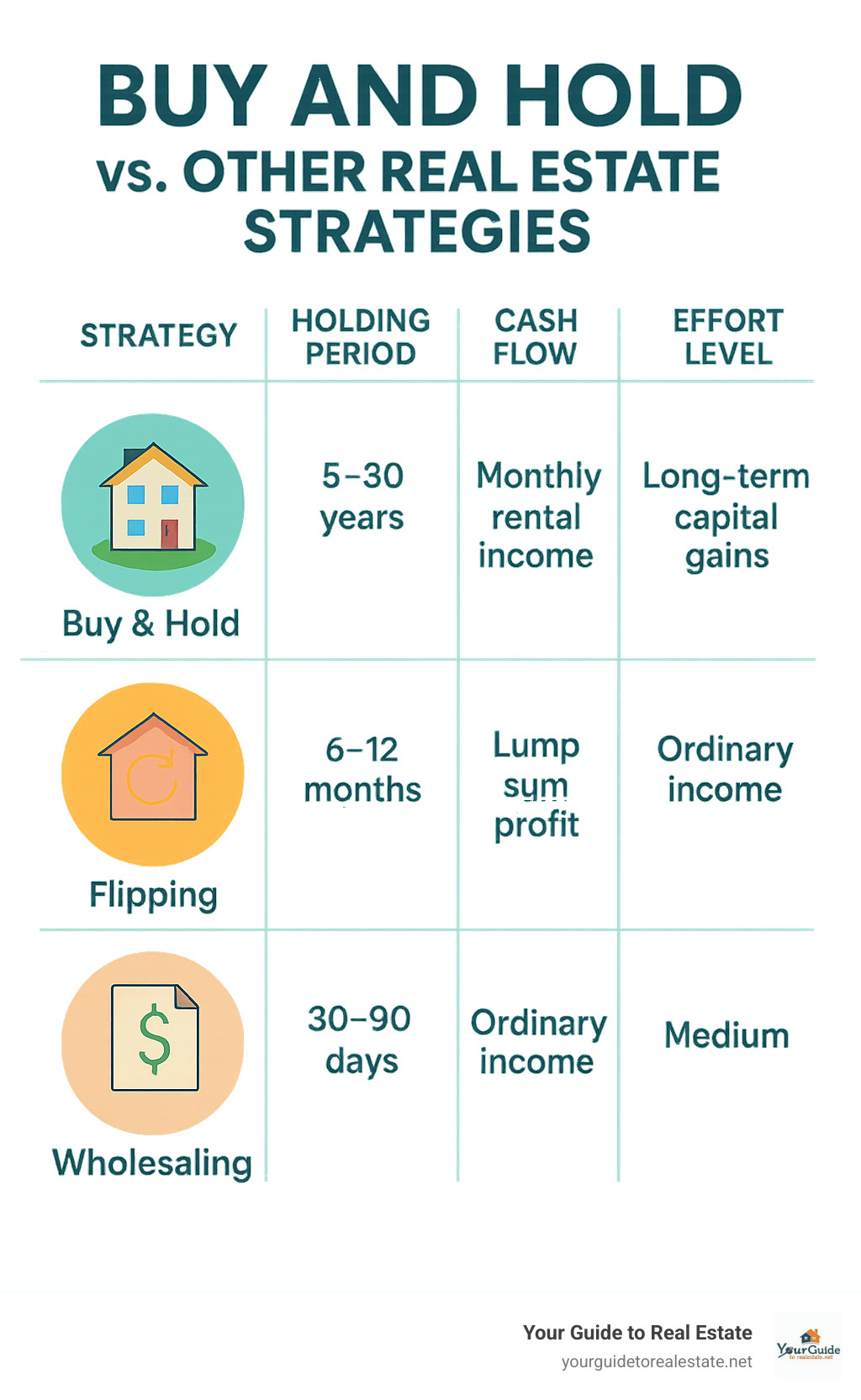

Buy and Hold vs. Other Real Estate Strategies

Flipping houses involves buying distressed properties, renovating quickly (6-12 months), and selling for profit. Requires construction knowledge and active management. Profits taxed as ordinary income.

Wholesaling means finding deals and assigning contracts to other investors for $5,000-15,000 fees. Requires constant deal-hunting. Assignment fees taxed as ordinary income.

REITs offer easy entry – buy shares like stocks and receive quarterly dividends. No property management but no control either.

Short-term rentals like Airbnb can generate 2-3 times traditional rent but require constant attention and face increasing regulations.

| Strategy | Holding Period | Cash Flow | Tax Treatment | Effort Level |

|---|---|---|---|---|

| Buy & Hold | 5-30 years | Monthly rental income | Long-term capital gains | Low-Medium |

| Flipping | 6-12 months | Lump sum profit | Ordinary income | High |

| Wholesaling | 30-90 days | Assignment fees | Ordinary income | Medium |

| REITs | Variable | Quarterly dividends | Dividend tax rates | Very Low |

Buy and hold real estate strikes a unique balance – monthly cash flow, long-term capital gains tax treatment, manageable effort level, and full control over your investments. It rewards patience over perfection and offers flexibility that other strategies don’t.

Taxes, Depreciation & Long-Term Wealth

The tax code is remarkably friendly to rental property owners. Depreciation allows you to deduct 1/27.5th of your property’s value (excluding land) each year as a “paper loss” that reduces taxable income, even if your property is appreciating.

Mortgage interest on investment properties is fully deductible. In early mortgage years, this can mean deducting $8,000-15,000 annually.

Operating expenses like property taxes, insurance, maintenance, property management fees, and mileage are all deductible business expenses.

The 20% Qualified Business Income (QBI) deduction allows you to deduct up to 20% of your rental income, subject to certain limitations.

Section 1031 exchanges let you defer capital gains taxes indefinitely by reinvesting sale proceeds into new investment properties.

When you combine these tax benefits with appreciation and cash flow, buy and hold real estate becomes a wealth-building machine. Many properties generate positive cash flow while showing paper losses for tax purposes.

Retirement income planning gets easier with multiple rental properties generating $500-1,000 each in monthly cash flow. That’s substantial retirement income plus valuable assets.

For comprehensive strategies, explore our guide on property investment.

Frequently Asked Questions About Buy and Hold Investing

How long should I plan to hold a rental?

At least one year for favorable tax treatment, but 5-10 years minimum for real wealth building. The one-year mark qualifies profits for long-term capital gains tax rates. The real magic happens in years 5-10 and beyond when mortgage balances drop significantly, rents increase with inflation, and property values compound.

What’s a healthy cash-on-cash return?

A healthy cash-on-cash return for buy and hold real estate typically falls between 6-12%. In expensive coastal markets, you might accept 4-6% returns betting on stronger appreciation. In affordable markets, 10-15% returns are often achievable with better monthly cash flow.

Cash-on-cash return is annual cash flow divided by total cash invested. Factor in appreciation, mortgage pay-down, and tax benefits for your total return.

Should I self-manage or hire a property manager?

Self-management maximizes cash flow but costs time and requires availability for tenant issues. Hire a property manager (8-12% of monthly rent) if you live far from rentals, own multiple properties, or want truly passive income.

Start by self-managing your first nearby property to learn the business, then consider professional management as you scale to 3-4 properties.

Conclusion

Buy and hold real estate isn’t about getting rich overnight – it’s about building wealth steadily until you have a portfolio generating serious passive income.

The strategy’s beauty lies in its simplicity. You don’t need construction expertise or marketing genius. You need patience, research skills, and discipline to stick with your plan when markets get bumpy.

Median home prices jumped 238% over 20 years while rental income flowed monthly. That’s the magic of combining cash flow with appreciation – you get paid while waiting for properties to grow in value.

The strategy harnesses powerful forces: leverage amplifies returns, tenants pay down mortgages, and inflation makes fixed-rate debt cheaper over time. You collect rent that often increases annually while mortgage payments stay the same.

Success requires balance. Stress-test your numbers, maintain proper reserves, and understand local landlord-tenant laws. The risks are real, but manageable with proper planning.

Start small and learn as you go. Your first property will teach you more than any book. Use that experience to refine your strategy, then gradually scale using equity and cash flow from your initial investment.

At YourGuideToRealEstate.net, we believe real estate investing should be accessible to everyone. Our mission is providing up-to-date guidance and educational resources that make complex investment strategies easier to understand and implement.

The path forward is straightforward: analyze your local market, get pre-approved for financing, and start looking for your first property. Don’t wait for perfect conditions – successful investors learn by doing.

For additional strategies to expand your real estate knowledge, explore our guide on Real Estate Business Growth.

The best time to plant a tree was 20 years ago. The second-best time is today. The same applies to buy and hold real estate – your future self will thank you for starting now.

")