Why Everyone’s Asking About Mortgage Rate Direction

Will mortgage rates go down? This question is on the minds of millions of potential homebuyers and existing homeowners across the country. After experiencing rates near historic lows of 2.65% in 2021, followed by a sharp climb to nearly 7.80% by late 2023, the mortgage market has been a rollercoaster ride.

Current outlook for mortgage rates:

- Short-term (2024-2025): Most experts predict rates will decline gradually, with forecasts ranging from 5.7% to 6.2% by end of 2025

- Key drivers: Federal Reserve policy, inflation trends, and economic growth

- Recent trend: Rates have already dropped from 2024 highs, with the 30-year fixed averaging around 6.5% as of late 2024

- Bottom line: Rates are expected to fall, but likely won’t return to pandemic-era lows

The recent decline has already made a difference. As Sam Khater, chief economist at Freddie Mac, noted: “Any time mortgage rate moves lower — even a small amount — we do see additional people who qualify to purchase a home.”

What’s driving the current trend? Several factors are pushing rates lower, including weaker economic data, slowing inflation, and investor expectations that the Federal Reserve will cut interest rates. The 30-year fixed-rate mortgage has seen some of its largest weekly drops in over a year.

But predicting mortgage rates isn’t simple. They don’t just follow Fed policy — they’re tied to complex factors like Treasury yields, mortgage-backed securities, and global economic conditions. Understanding these connections can help you make smarter decisions about when to buy, refinance, or wait.

Will mortgage rates go down glossary:

The Current Mortgage Rate Landscape

The mortgage market has been giving us quite a show lately, and the question “will mortgage rates go down” is becoming more hopeful by the week. We’re seeing some genuinely encouraging signs that rates are heading in the right direction.

Just recently, the 30-year fixed-rate mortgage took its biggest weekly tumble in over a year – dropping a full 15 basis points in one week. Then it happened again, with another 16-basis-point drop following a weaker August jobs report. That brought rates down to around 6.29%, the lowest we’d seen in months.

Right now, current 30-year fixed rates are hovering around 6.3% to 6.5% for borrowers with excellent credit. That’s down from the 6.75% we were seeing earlier this year. While these numbers change daily (and sometimes hourly), the trend is clearly moving in buyers’ favor.

The rate volatility we’ve experienced has been intense, but it’s starting to settle into a more predictable pattern. After months of uncertainty, experts are forecasting that rates will continue to stabilize and ease from their recent highs. You can track the latest official numbers through the Data on 30-year fixed-rate mortgages, and learn more about loan terms in our guide to 30-Year Mortgage Options.

How do today’s rates compare to the past?

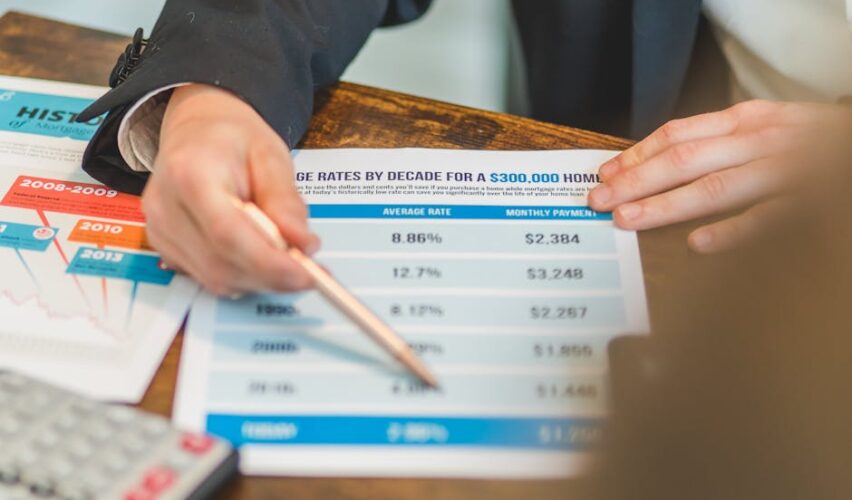

To really understand where we’re headed, let’s look at where we’ve been. The COVID-19 era rates were absolutely extraordinary – we hit an all-time low of 2.65% in early 2021. Those rates were like finding a unicorn in your backyard. They existed, but they weren’t going to stick around forever.

Then came the whiplash. By October 2023, rates had rocketed to nearly 7.79% – the highest we’d seen in decades. Talk about sticker shock! This dramatic swing left many potential buyers wondering if homeownership had suddenly become impossible.

But here’s some perspective that might surprise you: the historical average since 1971 for 30-year mortgages has been around 7.8%. That means today’s rates in the mid-6% range are actually closer to normal than those pandemic lows ever were. We’ve seen rates in double digits during the 1980s, so while 7% feels painful after experiencing 3%, it’s not historically unusual.

The bottom line? Those COVID-era lows were the exception, not the rule. While we’re unlikely to see 3% rates again anytime soon, the current trend toward the mid-6% range represents a return to more typical market conditions.

What factors are causing the recent dip?

So what’s driving this welcome change? The answer lies in several key economic shifts that are all pointing toward lower rates.

Weaker jobs reports have been a major catalyst. When that August employment report came in softer than expected, mortgage rates dropped 16 basis points in a single day. It might seem counterintuitive, but weaker job growth signals to investors that the economy might need support, which typically means lower interest rates ahead.

Slowing inflation is another big player. As inflation continues to cool down, the pressure on the Federal Reserve to keep rates high starts to ease. When the Fed doesn’t have to fight rising prices as aggressively, it creates room for rates to fall.

Investor sentiment has shifted dramatically. More investors are betting that the Fed will cut rates in the coming months, and this expectation is already being priced into the bond market. When investors expect lower rates, they’re willing to accept lower yields on bonds today.

The key relationship to understand is between mortgage rates and 10-year Treasury yields. Mortgage rates tend to track these Treasury yields closely, and when Treasury yields fall, mortgage rates usually follow. It’s like a dance where Treasury yields lead and mortgage rates follow a step behind.

For a deeper understanding of how these economic forces work together, check out our comprehensive guide on Understanding Mortgage Rates.

Key Economic Drivers of Mortgage Rates

Understanding whether will mortgage rates go down requires getting familiar with the economic forces that pull the strings behind the scenes. Think of it like watching a puppet show – the real action happens with the puppeteers you can’t see. In the mortgage world, those puppeteers are Federal Reserve policy, inflation, unemployment rates, Treasury yields, and the secondary mortgage market.

These aren’t just abstract economic concepts. They’re the daily drivers that determine whether you’ll pay 6% or 7% on your next home loan. When these forces align in certain ways, rates can drop dramatically in a matter of days. When they pull in different directions, we get the volatility we’ve been experiencing.

How do the Fed and Treasury yields affect rates?

Here’s something that surprises many people: the Federal Reserve doesn’t actually set mortgage rates directly. Instead, they work through the federal funds rate – essentially the interest rate banks charge each other for overnight loans. When the Fed raises this rate, borrowing becomes more expensive throughout the entire financial system, and that cost eventually lands on your mortgage application.

But here’s where it gets interesting. Mortgage rates are actually more closely tied to 10-year Treasury yields than to anything the Fed does directly. Why? Because mortgages get bundled into mortgage-backed securities (MBS) and sold to investors. These investors are constantly choosing between buying MBS and buying safer Treasury bonds.

When Treasury yields go up, investors demand higher returns from mortgage-backed securities to compensate for the extra risk. This pushes mortgage rates higher. When Treasury yields fall – like we’ve been seeing recently – mortgage rates typically follow them down.

The bond market is constantly trying to predict what the Fed will do next. Sometimes it gets ahead of itself, which is why you might see mortgage rates drop even before the Fed announces any policy changes. It’s like the market is saying, “We know what you’re going to do, so we’ll price it in now.”

One signal that really gets economists’ attention is an inverted yield curve – when short-term rates are higher than long-term ones. This unusual situation has historically predicted recessions within about 18 months, which often leads the Fed to cut rates aggressively. You can learn more about the Federal Reserve’s role in the economy.

What key indicators should you watch?

If you’re trying to time the market or just understand where rates might be heading, there are three key economic indicators worth following closely.

Inflation is the big kahuna. The Fed has committed to keeping inflation around 2% annually, and they’ll use interest rates as their primary weapon to achieve this. When inflation runs hot – like it did in 2022 when it peaked over 9% – the Fed raises rates aggressively to cool things down. As inflation has been steadily declining (it was down to 6% by February 2023), the pressure to keep rates high has been easing. This cooling trend is one of the main reasons experts are optimistic that will mortgage rates go down in the coming months.

Unemployment data tells us about the strength of the labor market, and it’s a bit of a double-edged sword. Strong employment usually means people have money to spend, which can fuel inflation. But a softening labor market – rising unemployment or slower job growth – often signals economic weakness, prompting the Fed to consider rate cuts to stimulate activity. Real estate experts like Danielle Hale watch employment reports closely because a cooling job market often precedes falling mortgage rates.

Gross Domestic Product (GDP) gives us the big picture of economic health. When GDP growth is robust, the economy might not need the stimulus of lower rates. But when growth slows – like the U.S. economy’s expansion cooling from 5.9% in 2021 to 2.1% in 2022, with even slower growth projected ahead – it creates conditions where rate cuts become more likely.

The beauty of watching these indicators is that they often move together. When inflation cools, unemployment might tick up, and GDP growth might slow – all pointing toward an environment where the Fed feels comfortable lowering rates. For a deeper dive into how these trends might play out, check out our Housing Market Forecast.

Expert Forecasts: Will Mortgage Rates Go Down?

The burning question will mortgage rates go down has economists, industry leaders, and homebuyers all looking into their crystal balls. While predicting mortgage rates isn’t an exact science, the consensus among experts paints a cautiously optimistic picture for the months ahead.

The good news? Most forecasters agree that we’re likely to see rates trend downward from their recent peaks. However, they’re also quick to remind us that the mortgage market can be as unpredictable as weather in springtime.

What are the predictions for the coming months and 2025?

Industry heavyweights are placing their bets on a gradual decline in mortgage rates, though they vary on just how far rates will fall. Fannie Mae expects the 30-year fixed mortgage rate to settle at 6.2% by the end of 2025, while the Mortgage Bankers Association (MBA) is slightly more optimistic at 5.9%. Morgan Stanley falls somewhere in the middle with their forecast.

The National Association of Home Builders predicts 5.94% by late 2025, and some bold predictions even suggest we could see rates touch 5% if economic conditions align just right. Looking ahead to 2026, Fannie Mae anticipates rates ending at 6.1%, while NAHB projects an even more favorable 5.69%.

What’s driving this optimism? Hector Amendola of Panorama Mortgage points to current economic conditions and signals from the Federal Reserve as reasons for expecting lower rates. Danielle Hale from Realtor.com echoes this sentiment, expecting rates to trend lower as markets anticipate Fed cuts. Even Tony Julianelle of Atlas Real Estate admits he’s “cautiously optimistic that mortgage rates will inch lower.”

But not everyone is ready to pop the champagne just yet. Sam Williamson of First American expects rates to hover in the mid-to-upper 6% range in the near term. He acknowledges that while Fed cut expectations are pushing yields down, inflation concerns could put a ceiling on how low rates can go.

For a deeper dive into what these trends mean for the broader market, check out our Real Estate Market Projections for 2025.

Are there opinions that rates might rise again?

Here’s where things get interesting – and a bit nerve-wracking for hopeful homebuyers. While most experts lean toward declining rates, several are waving yellow flags about potential bumps in the road.

Inflation remains the wild card that could derail the rate decline party. Despite recent cooling, inflation is still running above the Fed’s 2% target. If prices start heating up again unexpectedly, the Fed might slam on the brakes and delay those anticipated rate cuts. Selma Hepp, chief economist for CoreLogic, warns that expectations of higher government debt and deficits could keep Treasury yields – and by extension, mortgage rates – higher than many hope.

Government spending and fiscal policy add another layer of uncertainty. Richard Staniszewski, CEO of Hera Title, points out that elections and policy changes can inject serious volatility into markets. When the government borrows heavily to fund spending programs, it competes with mortgages for investor dollars, potentially pushing rates up.

Global events can also throw curveballs at mortgage rates. Rick Sharga, President/CEO of CJ Patrick Company, notes that we’re in “somewhat uncharted territory” when it comes to predictions, partly due to dramatic shifts in fiscal and monetary policy over recent years.

The bond market has its own personality too. Even if the Fed cuts rates, bond investors might demand higher yields if they’re worried about long-term inflation or government spending. It’s like having a mind of its own sometimes.

As Lawrence Yun, Chief Economist at the National Association of Realtors, wisely puts it: “While mortgage rates remain lifted, they are expected to stabilize.” But in mortgage rates, stability is always subject to change – sometimes faster than you can say “rate lock.”

The bottom line? Most experts believe will mortgage rates go down has a “yes” answer, but they’re keeping their expectations realistic about how far and how fast that decline might happen.

How Lower Rates Impact Homebuyers and the Market

When people ask “will mortgage rates go down,” they’re really wondering about something much bigger – how those changes will affect their dreams of homeownership and the housing market as a whole. The good news is that even modest drops in rates can create meaningful opportunities for buyers and sellers alike.

What does this mean for housing affordability?

Lower mortgage rates are like getting a discount on your biggest purchase. The impact on your wallet is both immediate and long-lasting, making homeownership more accessible in several key ways.

Monthly payment savings represent the most tangible benefit you’ll see right away. Even what seems like a small rate drop can translate to significant monthly savings. Picture this: on a $450,000 home, a rate drop from 7% to 6.29% could save you approximately $169 every month. If you’re looking at a $1 million home, that same kind of shift from 7% to 6.25% could mean $397 less in monthly payments.

Over the life of a 30-year mortgage, these numbers become even more impressive. The difference between a 7% and 6% mortgage rate on a median-priced home amounts to $274 per month – that’s $3,288 annually that stays in your pocket instead of going to interest.

Increased purchasing power is another game-changer. When your monthly payments are lower, you can afford to borrow more money for the same monthly budget. This effectively expands your options, potentially opening doors to neighborhoods or homes that were previously out of reach.

However, there’s a catch to consider. Lower rates tend to boost demand, which can create upward pressure on home prices. For real affordability gains, we’d ideally see both dropping mortgage rates and slower price growth – or even modest home price declines.

The challenge is that average home prices have climbed approximately 30% since early 2020, and we’re still dealing with a shortage of homes for sale. According to CoreLogic’s chief economist Selma Hepp, this means any price declines are expected to be modest at best.

How will the housing market react?

The housing market has a way of responding quickly to rate changes, often creating a ripple effect that touches buyers, sellers, and the overall inventory.

Increased buyer activity typically follows rate drops like clockwork. When borrowing becomes more affordable, previously sidelined buyers suddenly find themselves back in the game. We’ve already witnessed this phenomenon – purchase applications recently hit their highest year-over-year growth rate in more than four years following recent rate dips.

As Lawrence Yun from the National Association of Realtors explains, “Any time mortgage rate moves lower — even a small amount — we do see additional people who qualify to purchase a home.” It’s that simple and that powerful.

More homes hitting the market is another welcome side effect. Many homeowners have been stuck in what experts call the “lock-in effect.” These folks secured ultra-low rates during the pandemic and have been reluctant to sell because they’d have to take on a new mortgage at much higher rates.

When rates come down significantly, it suddenly becomes more financially practical for these homeowners to make a move. This can help invigorate what has been a sluggish housing market by increasing the inventory of available homes.

For homeowners who bought during the recent high-rate period, falling rates present prime refinancing opportunities. This could mean lower monthly payments, reduced total interest over the loan term, or even a chance to tap into home equity. If you’re curious about how this process works, our guide on Mortgage Refinancing Explained breaks it down in simple terms.

The bottom line? Falling mortgage rates can inject fresh energy into a stalled housing market, potentially creating a more balanced environment where both buyers and sellers have better opportunities to achieve their goals.

Strategies for Homebuyers in a Fluctuating Rate Environment

The question of “will mortgage rates go down” is important, but it shouldn’t paralyze your homeownership dreams. In a fluctuating rate environment, the best strategy is to focus on what you can control. Our proven framework and stress-free guidance at Your Guide to Real Estate emphasize personal financial readiness over trying to time the market perfectly.

What can you do while waiting for mortgage rates to go down?

While we eagerly await further rate declines, there are several actionable steps you can take to put yourself in the best possible position:

- Improve Your Credit Score: A higher credit score signals to lenders that you are a lower-risk borrower, which can qualify you for better interest rates regardless of market fluctuations. We recommend regularly checking your credit report for errors and consistently making on-time payments.

- Automate Savings for a Down Payment: The more you can put down upfront, the less you’ll need to borrow, which can lead to a lower interest rate and more manageable monthly payments. Setting up an automated savings plan can help you build your down payment steadily.

- Reduce Your Debt-to-Income (DTI) Ratio: Lenders look at your DTI to assess your ability to manage monthly payments. A lower DTI can make you a more attractive borrower and potentially open up better rates. Focus on paying down high-interest debts.

- Get Pre-Approved: This is a crucial step. A mortgage pre-approval gives you a clear understanding of how much you can afford and demonstrates to sellers that you are a serious buyer. It also allows you to lock in a rate for a certain period, protecting you if rates rise during your home search. Being pre-approved means you’ll be ready to move quickly when you find the right home, a significant advantage in today’s market.

You don’t have to put your life on hold. Many buyers choose to purchase now, secure in the knowledge that they can always refinance later if rates drop further. Starting to build equity today can be a powerful financial move. For more guidance, check out our First-Time Homebuyer Tips.

How do you find the best possible rate today?

Even when rates are generally trending down, the rate you actually receive can vary significantly. Here’s how to ensure you’re getting the best possible deal:

- Comparing Lenders is Key: This is perhaps the most impactful step. Don’t just go with the first offer you receive. Shopping around and getting quotes from multiple lenders (we recommend at least 3-5) can lead to substantial savings. Studies show that getting quotes from just four lenders can save you around $1,200 annually on a mortgage. This is where our expertise comes in, helping you steer the options.

- Understand the Loan Estimate: Once you apply for a loan, lenders are required to provide a Loan Estimate, which details the interest rate, monthly payment, and closing costs. Compare these documents carefully. Don’t just look at the interest rate; consider the Annual Percentage Rate (APR), which includes fees and the interest rate, giving you a more comprehensive picture of the total cost of borrowing.

- Consider Discount Points: These are upfront fees you pay to the lender in exchange for a lower interest rate over the life of the loan. One discount point typically costs 1% of the loan amount. You need to calculate if the long-term savings from the lower rate outweigh the upfront cost, especially considering how long you plan to stay in the home.

- Explore Rate Buydowns: A rate buydown is a payment made at closing to temporarily reduce the interest rate for the first few years of the loan. This can be a great option if you expect rates to fall further, allowing you to benefit from lower payments initially while waiting for a good time to refinance.

By actively engaging in these strategies, you can secure the most favorable terms available, regardless of whether will mortgage rates go down further tomorrow. For a comprehensive guide on this process, read our article on How to Shop Mortgage.

Conclusion

The journey to homeownership or refinancing in today’s market naturally leads to one burning question: “will mortgage rates go down?” After exploring the economic indicators, expert predictions, and market dynamics that shape rates, here’s what really matters: focus on what you can control.

It’s tempting to play the waiting game, trying to time the perfect moment when rates hit rock bottom. But as we’ve seen throughout this guide, mortgage rates are like weather patterns – influenced by countless unpredictable factors from inflation surprises to global events. The experts we’ve consulted generally agree that rates will likely decline gradually, but nobody can guarantee exactly when or by how much.

Your personal financial readiness is far more powerful than perfect timing. When you strengthen your credit score, build a solid down payment, and reduce your debt-to-income ratio, you’re creating opportunities regardless of market conditions. These strategies work whether rates are at 6%, 7%, or even if they drop to 5%.

At Your Guide to Real Estate, we’ve guided countless families through uncertain rate environments using our proven framework. Our philosophy often comes down to this simple wisdom: “marry the house, date the rate.” If you find a home that fits your life and budget at current rates, don’t let the possibility of future rate drops hold you back from building equity today.

Your long-term homeownership goals shouldn’t be held hostage by short-term market fluctuations. You can always refinance later if rates drop significantly. But you can’t go back in time to start building equity sooner or to secure that perfect home that got away.

The truth is, there’s never a “perfect” time to buy – there’s only the right time for you. With proper preparation and expert guidance, you can make confident decisions that align with your personal situation, regardless of what tomorrow’s rates might bring.

Ready to take control of your homeownership journey? Get our beginner’s guide to understanding mortgages and let us provide the stress-free guidance you need to steer your path to homeownership successfully.

")